As shared last week on this blog, I have tried to pursuade the board of Karelia Tobacco, that the company and its (minority) shareholders would benefit from a stock split. The identification of a liquidity problem and a proposed solution are detailed in my letters (found below), and I will therefore not go into repetition by going over it in this short little intro. I will say this about the proposal:

- I am not criticizing management in any way; quite the opposite in fact, because I believe they have done an excellent job in a difficult environment.

- I am not proposing any change in management, oversight, capital returns policy, or anything else about the way the Karelias family manages their company.

- My proposal instead aims to solve (or alleviate) a real problem that hurts minority shareholders in a very significant way. The cost to the company in terms of time and monetary expense is very moderate and much proportionate to the benefits expected to arise for its shareholders.

I therefore believe my proposal is both reasonable in its scope and rational in its content. Sadly, my first two letters went unanswered, which is perhaps to be expected, but I still decided to follow up with a third letter (sent last week). I have reached out to some other bloggers in order to drum up some support for my proposal and now I am putting the letters up for everyone to see. If you are a shareholder yourself, please feel free to use the last letter, sign your own name to it and sent it in (to info@karelia.gr) with the request that it be delivered to the board (you can also reach out to me). Better make it soon though: the agenda for the AGM can probably be expected shortly. I am still weighing the benefits of attending the company’s upcoming meeting of shareholders.

Third Letter – Spring 2016

For the attention of: Board of Directors

Victoria C. Karelia

Andreas G. Karelias

Efstathios G. Karelias

Vassilios G. Antonopoulos

Robin D. Joy

Karelia Tobacco Company Inc.

Via email to: info@karelia.gr

Athinon Street

241 00 Kalamata, Greece

May 12th 2016

Dear Lady and Gentlemen:

As a shareholder of Karelia Tobacco, I have taken the liberty to write this letter in order to bring some items to the attention of the company board. First of all, let me congratulate you on the strong performance achieved by the company during 2015. I have no doubt that significant efforts have been required from both management and employees to achieve such a sizeable increase in revenues and margins. I know you have expressed some conservatism in your forward-looking comments, included in your latest financial statements, but I have some hope of seeing another strong performance in 2016. My main reason for writing this letter is, however, something other than a discussion of operational achievements, however much these are worthy of praise. No doubt you may know by now what I am referring to, namely the ever-present discount to intrinsic value at which your share continues to trade. I have brought this to your attention on two earlier occasions, but sadly the problem persists. If I held the conviction that the problem was unsolvable, I would not go to these lengths to bother you with it, but since the problem is both serious in its impact and entirely solvable, I feel I have little choice but to continue addressing it.

In my opinion, the illiquid nature of Karelia’s stock listing continues to cause its stock to trade at a significant discount to any rational valuation of its business. As I have stated earlier, I believe that a stock split can serve to solve, or at least alleviate, this problem by lowering the nominal value while increasing the tradeable number of shares. Improved liquidity will probably lead to an upwardly revised stock price, which would help shareholders who elect to sell in realizing a fair value for their holdings. And what after all are shareholders other than partners in a business? One partner may hold a substantially larger piece of a business than his fellow shareholder, but they are partners nonetheless. Should partners not ensure that any other partner, even one who is giving up his ownership, can realize the value of his holdings at something close to the business’s underlying worth? It is my opinion that partners should indeed care to realize such an outcome, if at all possible. As members of Karelia’s board, appointed as company overseers by the shareholder’s assembly, I assume you feel this responsibility and take it seriously. In fact, I know you do because it is included in the company’s corporate governance code; “Moreover, the fair and equitable treatment of all shareholders should be ensured, including minority shareholders and foreign shareholders”. The company’s commendable actions regarding its dividend payment, amidst the advent of capital controls last year, confirm my belief that you do indeed care deeply about upholding this principle. I greatly appreciated the way I was informed on the course of action taken to ensure timely payment, and realize that it has been the actions and guidance of Karelia’s management and board that have established the sound footing from which the company was able to keep its promise. For this I would like to thank you.

I therefore believe I can convince you of taking action regarding the irrational pricing behavior in the share price as well. In my opinion, there are at least three strong indications that pricing action in Karelia’s stock suffers from the consequences of low liquidity, caused at least in part by a high nominal value and a low free float. The first indicator is the fact that Karelia consistently sells at a huge discount to its international tobacco sector peers. In the table below I have included a list of consumer tobacco companies listed on public markets. All of these companies sell at significantly higher multiples of earnings than Karelia, with the discount versus the trailing sector price/earnings multiple at least 40%. I should also add that this is on the basis of Karelia’s reported earnings; the discount is substantially larger if instead we used underlying earnings (adjusted for the legal charge taken against earnings).

Table above includes data from the Yahoo! Finance website for all companies except Karelia Tobacco (for which I relied on reported financials).

The second indicator for irrational pricing action in the share of Karelia Tobacco’s is the regular occurrence of inverted bid/ask spreads. I have included screenshots from 6 instances in which this occurred, but I can testify to the fact that it has happened more often. I believe the irrationality of an inverted spread is quite obvious: the seller is after all pricing his shares below the highest current offer, thereby directly damaging his own financial interest.

Above: On the 26th of February 2015 the bid/ask in the share showed an inverted spread of more than 5%.Screenshot taken around 11:52 AM local time of the stock’s profile page on Helex.gr.

Above: On the 18th of August 2015 the bid/ask spread was a negative 11%. Screenshot taken around 12:02 PM local time of the stock’s profile page on Helex.gr.

Above: On the 5th of November 2015 the stock’s bid/ask was a negative 4.3%. Screenshot taken around 12:02 PM local time of the stock’s profile page on Helex.gr.

Above: On the 9th of December 2015 the stock’s big/ask was a negative 4%. Screenshot taken around 14:59 PM local time of the stock’s profile page on Helex.gr.

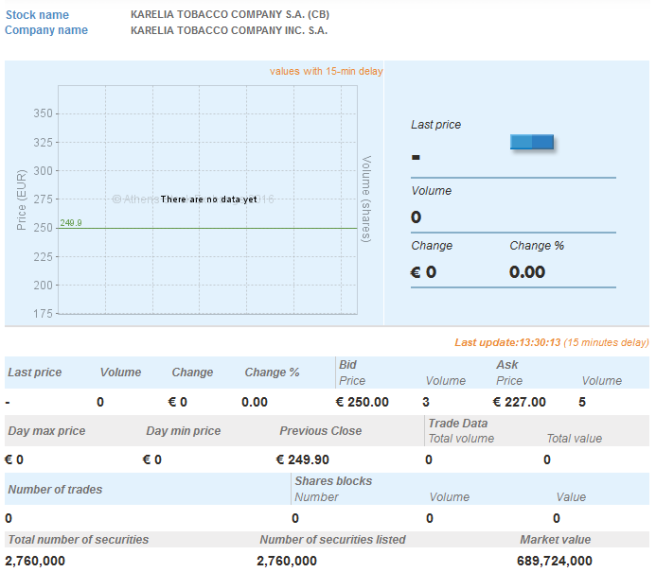

Above: On the 20th of January 2016 the stock’s bid/ask spread was a negative 5.9%. Screenshot taken around 15:39 PM local time of the stock’s profile page on Helex.gr.

Above: On the 21st of April 2016 the stock’s bid/ask spread was a negative 10.1%. Screenshot taken around 14:30 PM local time of the stock’s profile page on Helex.gr.

The third indicator of irrational pricing action in Karelia Tobacco’s share is the regular occurrence of excessive price movements. I have included a particularly striking example below.

On the 29th of December 2015 there were some highly unusual fluctuations in the company’s share price. The stock dropped by €40 (-15.69%) versus the last recorded transaction price on volume of 24 shares.

By 13:43 PM another transaction involving 25 shares had taken place at €230 per piece.

Then, by 15:59 PM another 26 shares had changed hands, this time at €226.

At the end of the day, the stock closed at €235.95 due to a transaction involving another 30 pieces.

Only one day later, on December 30th 2015, the stock traded 2 pieces at €231 and 93 pieces at €250.

The example above shows that within a period of 24 hours, the valuation assigned by the market to Karelia Tobacco fluctuated by roughly 16.3%, on no news whatsoever. This constitutes a valuation difference of €96.6 million in the company’s market capitalization, which seems highly undesirable to me. If we take the example of the shareholder who sold 24 pieces on the morning of December 29th 2015, and assuming the €250 price is the more rational one, his gross proceeds were impaired by €840 (24x€35 difference). This may not seem like a lot but will add up to very significant sums over years, which directly impacts the financial results a selling shareholder achieves from his investment in Karelia. In this particular example his proceeds could have been higher by 16.3%, or almost 4.5x current net annual dividends of €7.65. I believe we can all agree that this type of stock price behavior is far from rational, highly undesirable and something that should be addressed.

A stock split, ideally one with a high denominator, would in my opinion serve to reduce the irrational pricing by narrowing the bid/ask spread, increase the chances of daily pricing and allow investors to benefit from the improved liquidity a higher number of outstanding shares can provide. The effect of stock splits has been well researched by the academic world and it has been reasonably well established[i] that there is a meaningful benefit with regards to liquidity and pricing. I therefore propose that the board of Karelia Tobacco acts to alleviate the negative consequences minority shareholders continue to suffer from the low liquidity in its stock listing.

[i] For examples see ‘Liquidity Changes Following Stock Splits’, Copeland, T.E, The Journal of Finance, Vol. XXXIV, no.1, March 1979 as well as ‘Liquidity and Stock Returns’, Amihud, Y. and Mendelson, H., Financial Analysts Journal, May/June 1986, Vol.42, Issue 3. Other examples are ‘Investor Relations, Liquidity and Stock Prices’, Brennan, M.J. and Tamarowski, C., Journal of Applied Corporate Finance, Vol.12, Issue 4, January 2000, pg. 26-37 as well as ‘Long-Run Common Stock Returns Following Stock Splits and Reverse Splits’, Desai, H. and Jain, P.C., The Journal of Business, vol.70, no.3, July 1997, pg. 409-433.

Second Letter – Spring 2015

Board of Directors

Karelia Tobacco Company Inc.

Via email to: info@karelia.gr

Athinon Street

241 00 Kalamata

Greece

Attention:

Victoria C. Karelia (Chairwoman)

Andreas G. Karelias (Managing Director)

Efstathios G. Karelias (Vice Chairman)

Vassilios G. Antonopoulos (Member)

Robin D. Joy (Member)

June 11th 2015

Dear Lady and Gentlemen:

This letter is a follow-up on my earlier message dated October 24th 2014 in which I addressed an issue regarding the trading of your share on the Hellenic Stock Exchange. Unfortunately I have not received a reply or witnessed a modified course of action initiated by you, constituting the board of directors of Karelia Tobacco. Since my earlier letter was send only to the general e-mail account mentioned as contact information on the investor relations page of your website, there is a possibility that my message never reached its destination. Another possibility is that you disagree or fail to see the benefits inherent in my proposal for a stock split. With the Annual General Meeting of shareholders due to take place within a week’s time I have taken the effort to raise the issue with you once more. Reading through the materials published with regards to this meeting I noticed shareholders who succeed in assembling a 5% minority interest behind a certain proposal can, according to your bylaws, request that it be placed on the agenda of the shareholder meeting. According to my information however, the extended Karelias family either directly or indirectly controls about 94.48% of total shares outstanding. Since this leaves only a 5.52% interest in the hands of public shareholders, the chances of either controlling a sufficiently large interest or gaining the support of those who on a cumulative basis own such an interest is exceptionally small. Since I do not have the votes to require the admission of my proposal on the agenda I will try, in an effort to change your mind, to make a convincing case to you once more regarding the benefits of a stock split.

In my October letter I focused mostly on the interests of selling shareholders, who may not get a fair price due to the current undervaluation of your share. I still believe your share to be significantly undervalued and this argument therefore still stands. However, the Greek stock market as a whole trades at depressed levels due to reasons well-known to all with a vested interest. Liquidity has also been drained from the Hellenic Exchange due to the long-lasting uncertainties caused by the current level of stress in the Greek government’s fiscal position. Obviously, this is an issue outside your control and responsibility. I concede that this situation may have caused lower levels of liquidity in Karelia Tobacco’s shares as well. However, regarding the low level of free float and the high nominal value of Karelia shares I still think a notable improvement could be gained from executing a stock split. In my letter from October I mentioned a stock split could be performed through issuing a stock dividend on the existing share count. As you are probably aware this may cause accounting problems in case Greek law prohibits the issuance of shares below their nominal book value. In order to avoid such an issue a stock split can also be performed by actually splitting the existing shares into more shares with a lower nominal value, thereby avoiding a stock issuance.

Perhaps you consider the current situation not in need of change, which I can understand to a certain degree. I would like to direct your attention to the possibility that Karelia itself might benefit from having a more highly traded share. With the Greek market having become, to a certain degree, a stock market with a great many ‘penny stocks’ and a relatively small amount of stocks of large capitalization, your company’s share may become eligible for promotion to certain indices of the Greek stock market. Even with only slightly over 5% of the company’s share count in public hands the free float would, at the present market capitalization, constitute over €30 million. That may be enough, depending on liquidity, to grant Karelia a place in a stock index such as the ATHEX. The benefit to Karelia would be an increase in status and visibility of the company and its products, which may help it gain more recognition with potential customers and with consumers of tobacco products. In my opinion this could be beneficial to the company, which due to the advertising limitations on tobacco products has limited possibilities for increasing the awareness and visibility of its products. A more visible stock listing would in my opinion contribute to an elevation of the company’s profile among potential customers. The retail establishments that sell your products are oftentimes part of large retail companies that may have a public stock listing as well. Many of your competitors meanwhile already enjoy a highly visible status through being a part of consolidated tobacco companies such as Philip Morris or Japan Tobacco. Improved visibility of your status as a listed and well-performing company could in my opinion add to your image of being a trustworthy and strong potential business partner. Some relatively small expenditures on outside consultants or regulatory measures aside, this added visibility has the potential to function as a form of free publicity, which should be attractive to any company. It could also raise your profile among domestic consumers, which may at this point be sensitive to supporting Greek industry through their consumption. Awareness of your company’s status as an independent Greek business and job provider could be exploited as a strength in the Greek tobacco market for instance.

Concluding my arguments I would like to say that a stock split should benefit both shareholders and the company itself, which of course are both important for you to consider as board members. I hope you will reconsider my proposal regarding a stock split, perhaps as soon as on the AGM one week from now.

First Letter – Fall 2014

Board of Directors

Tobacco Industry Karelia A.E.

Via email to: info@karelia.gr

Athinon Street

241 00 Kalamata

Greece

Attention:

Victoria C. Karelia (Chairwoman)

Andreas G. Karelias (Director)

Efstathios G. Karelias (Vice Chairman)

Vassilios G. Antonopoulos (Director)

Robin D. Joy (Director)

24th October 2014

Dear Lady and Gentlemen:

As a shareholder of your company I would like to address an issue regarding the current way in which your stock trades on the Athens Exchange. Allow me to start by saying the following; I have been reading up on your company from the time of my investment, mostly through reading your annual reports of the past years. Unfortunately I do not speak or read Modern Greek so I have had to rely on translated versions of your quarterly reports to catch up with the latest developments. From what I have learned my impression is that Karelia Tobacco is a good business that has been managed well throughout the years. Especially since tough competition and harsh conditions on your domestic market have made your company’s operating environment quite challenging. I’m impressed by the way you’ve handled these circumstances by focusing more on exports and emphasizing innovation. If my information is correct Karelia has been able to claim a meaningful share of the Bulgarian cigarette market since its liberalization and is currently the largest international player on the market. Your strongly risen exports to the markets of North Africa have also captured my eye. All things considered I’m quite satisfied with the way Karelia is being run. To paraphrase American investor Warren Buffett: your company seems to be “a high class business run by high-class people”. I hope you understand therefore that this letter is not in any way intended to criticize management or oversight of the company.

As stated, the issue I want to bring to your attention is the reservations I have about the way your stock is traded on the Athens Exchange. You will be aware that trading activity in Karelia’s shares is very thin or even sporadic, with sometimes no daily volume traded at all. It has struck me that the spread between bid and ask prices is oftentimes very large, which is related to these low levels of liquidity. The result of this is that the stock can swing quite wildly on any given day, due to mismatches in supply and demand. The problem this causes in my perception is that current shareholders may be forced to accept prices that do not reflect the underlying value of your company. Karelia shares currently trade near €200, which constitutes a meaningful discount to fair value*. In my opinion the current undervaluation of the stock is unrelated to operating performance but is due to low liquidity, which is an issue that is at least partly addressable. The action I propose is intended to increase the volume traded while at the same time reducing bid and ask spreads. I think this can be achieved by means of a stock split, which will increase the number of shares outstanding while lowering the nominal price of individual shares. Splitting a company’s stock, usually by way of a stock dividend, of course does not change a shareholder’s percentage ownership in the company and will not alter or erode in any way the family-controlled nature of the company. My proposal is to issue a 39 shares stock dividend to current shareholders, effectuating a 40-1 stock split that would reduce the (current) share price from around €200 to around €5 per share, while increasing the outstanding share count to 110.4 million. I am aware of the low free float in the share base, given the substantial holdings by Karelias family members. In my opinion however both a lower nominal price of the stock and the larger total share count should improve daily trading volumes as well as lead to more rational pricing action. This will then hopefully reduce the chance of existing shareholders that wish to sell being forced to accept prices that significantly undervalue their holdings. I hope you will evaluate this proposal and consider taking action. I look forward to hearing from you.

*My estimate of fair value is based on the average multiple paid in tobacco company buy-out transactions over the past 15 years. For an average multiple of 12x EV/Ebitda my estimate of your company’s underlying value would be €293 per share excluding net cash holdings or €355 including cash, implying a discount of 46.5% – 77.5% for the shares of your company at the current share price of €200.

Don’t expect a reply. Ever. The Karelia family is entirely uninterested in the shares. If they would ever answer, the message would likely urge you to find something else to follow. They are owners and have a horizon that spans decades.

LikeLike

Do you have any experience with the company? As regards their lack of communication; I think I got that message (not so) loud and clear. Nevertheless, I still think a public company should maintain a certain minimum level of responsiveness. Otherwise they should be entirely private. The current state of affairs is also in direct contradiction with their own governance code.

LikeLike